U.S. Tax Residency vs Indian Residential Status: A Complete Guide for Indian Accountants

If you’re an Indian accountant planning to learn U.S. taxation, the very first concept you must understand is tax residency.

Before calculating tax, claiming deductions, or deciding which tax return to file, both India and the United States ask one fundamental question:

“Is this individual a tax resident?”

The answer determines:

- Which income is taxable

- Which tax return should be filed

- Whether worldwide income must be reported

- Which deductions, exemptions, and tax benefits are available

Although both countries determine residential status before computing income tax, the rules are completely different.

Many Indian accountants make the mistake of assuming the U.S. follows the same approach as India. It doesn’t.

In this guide, you’ll learn:

- How India determines residential status

- How the United States determines tax residency

- The biggest differences between the two systems

- Practical examples

- Common mistakes beginners make

Let’s begin.

Why Residential Status Matters

Residential status is one of the most important concepts in taxation.

It determines the scope of taxable income.

For example:

Two individuals may earn exactly the same salary.

However, one may be taxable on worldwide income, while the other may be taxable only on income earned within that country.

That is why determining residential status is always the first step in tax computation.

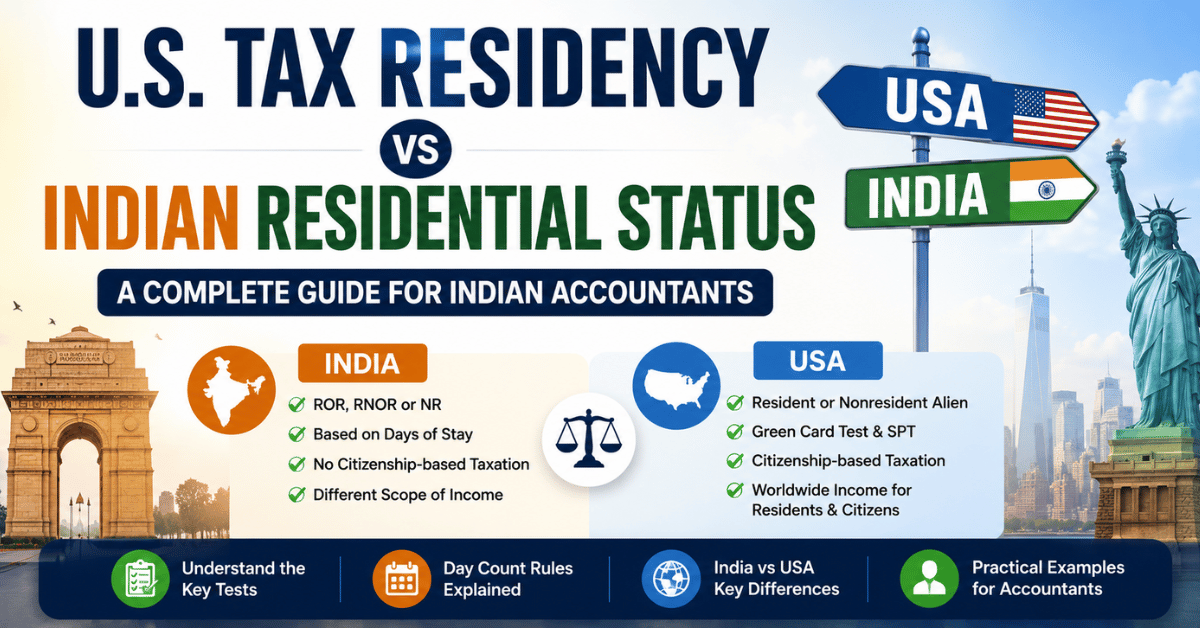

How India Determines Residential Status

Under the Indian Income-tax Act, residential status is determined primarily by physical presence in India during the relevant financial year and preceding years.

The process generally has two steps.

Step 1 – Determine Whether the Individual Is Resident

An individual is first tested against the basic conditions prescribed under the Income-tax Act.

If neither condition is satisfied, the individual is treated as a Non-Resident (NR).

If at least one basic condition is satisfied, the individual becomes a Resident.

Step 2 – Determine the Category of Resident

If an individual qualifies as a resident, additional conditions are examined to determine whether the person is:

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

Therefore, India has three residential categories:

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

- Non-Resident (NR)

How the United States Determines Tax Residency

Unlike India, the United States has only two primary tax residency categories.

- Resident Alien

- Nonresident Alien

However, the method used to determine residency is completely different.

The IRS generally uses two tests.

1. Green Card Test

The first test is the Green Card Test.

If an individual is a lawful permanent resident of the United States (commonly known as a Green Card holder), the individual is generally treated as a Resident Alien for U.S. tax purposes.

Unlike India, the number of days spent in the United States is generally not the deciding factor once the Green Card Test applies.

2. Substantial Presence Test (SPT)

If the individual is not a Green Card holder, the IRS generally applies the Substantial Presence Test (SPT).

Unlike India, the U.S. does not simply count the number of days spent in the current year.

Instead, it considers physical presence over three calendar years using a weighted formula.

To satisfy the SPT, an individual generally must:

- Be physically present in the U.S. for at least 31 days during the current year, and

- Have a weighted total of 183 days over the current year and the previous two years.

The formula is:

Current Year Days

- 1/3 × Previous Year Days

- 1/6 × Second Previous Year Days

If the total equals or exceeds 183 days, the individual generally satisfies the Substantial Presence Test.

Example

Suppose Rahul stayed in the United States:

Current Year – 160 days

Previous Year – 120 days

Second Previous Year – 120 days

SPT Calculation:

160

- 40

- 20

= 220 Days

Since the weighted total exceeds 183 days and Rahul meets the minimum current-year presence requirement, he generally satisfies the Substantial Presence Test.

Does Meeting the Substantial Presence Test Always Make You a Resident?

No.

This is one of the biggest differences between learning U.S. taxation and Indian taxation.

Even after satisfying the Substantial Presence Test, an individual may still be treated as a Nonresident Alien if they qualify for certain exceptions.

Examples include:

- The Closer Connection Exception

- Relief under an applicable income tax treaty

- Certain special rules applicable to eligible foreign students

This surprises many Indian accountants because there is no direct equivalent under Indian residential status rules.

The Biggest Difference: Citizenship

Perhaps the most significant difference between India and the United States is citizenship-based taxation.

India

India does not tax individuals merely because they are Indian citizens.

If an Indian citizen qualifies as a Non-Resident under the Income-tax Act, their foreign income is generally not taxable in India merely because they hold Indian citizenship.

Residential status—not citizenship—is the primary factor in determining the scope of taxation.

United States

The United States is different.

The U.S. generally taxes:

- U.S. Citizens

- Resident Aliens

- Green Card Holders

on their worldwide income, regardless of where they live.

This means a U.S. citizen living in India, Dubai, Australia, or Singapore may still have U.S. tax filing obligations even if they have not lived in the United States during the year.

This concept is unique and is one of the defining characteristics of the U.S. tax system.

Example

Consider two software engineers working in Dubai.

Rahul

- Indian Citizen

- Qualifies as a Non-Resident under Indian tax law

Generally, Rahul’s Dubai salary is not taxable in India merely because he is an Indian citizen.

John

- U.S. Citizen

- Lives and works in Dubai

John may still be required to file a U.S. tax return and report his worldwide income to the IRS, although provisions such as the Foreign Earned Income Exclusion, Foreign Tax Credit, or applicable treaty rules may reduce double taxation.

This single example highlights one of the biggest philosophical differences between the two tax systems.

India vs USA – Residential Status Comparison

| Particulars | India | United States |

|---|---|---|

| Number of residential categories | ROR, RNOR, NR | Resident Alien, Nonresident Alien |

| Primary basis | Physical presence in India | Green Card Test and Substantial Presence Test |

| Uses weighted three-year formula | No | Yes |

| Green Card concept | No | Yes |

| Equivalent of RNOR | Yes | No |

| Citizenship creates worldwide tax liability | No | Generally yes, for U.S. citizens |

| Worldwide income taxable | Generally for ROR | Generally for Resident Aliens and U.S. citizens |

| Tax treaties may affect residency | Yes | Yes |

| Special exceptions after meeting day-count rules | Limited | Yes |

Common Mistakes Indian Accountants Make

1. Assuming Visa Status Determines Tax Residency

Immigration status and tax residency are not the same.

A visa alone does not determine whether an individual files Form 1040 or Form 1040-NR.

2. Ignoring the Green Card Test

Many beginners focus only on counting days.

However, the Green Card Test is an independent residency test.

3. Assuming the Substantial Presence Test Is the Final Step

Even after satisfying the SPT, exceptions such as the Closer Connection Exception or treaty provisions may still apply.

4. Applying Indian Residential Rules to U.S. Taxation

The concepts are similar, but the legal framework is entirely different.

Understanding India’s residential status rules does not automatically mean you understand U.S. tax residency.

Why This Concept Matters for Form 1040

Before preparing any U.S. individual tax return, the first question should always be:

“Is the taxpayer a Resident Alien or a Nonresident Alien?”

The answer determines whether the taxpayer generally files:

- Form 1040, or

- Form 1040-NR

Without determining tax residency correctly, the entire tax return may be prepared using the wrong rules.

Final Thoughts

Residential status is the foundation of both Indian and U.S. income taxation.

However, the two countries follow very different approaches.

India focuses primarily on physical presence and classifies taxpayers as ROR, RNOR, or NR.

The United States relies on the Green Card Test, the Substantial Presence Test, and, uniquely, also taxes its citizens on worldwide income, even if they live outside the U.S.

For Indian accountants entering the field of U.S. taxation, mastering this concept first will make every other topic—from Form 1040 and Form 1040-NR to tax treaties and international taxation—much easier to understand.

If you can confidently determine a taxpayer’s residency status, you’ve already mastered one of the most important foundations of U.S. individual taxation.